Just when you get set to write a long boring piece filled with doom and gloom the US market goes and puts on its best day since August 2015. Just as well I held off:

a) writing that note (yet) and

b) panicking and taking emergency protective positions.

Regardless the markets have had a week best described as ‘odd’ with many fingers pointing in many directions on numerous reasons. Trade war commentary has been done to death and will be flogged for a while to come. I’ll do my best to add a few cents below too.

However one of the things that crept sneakily under the radar of many commentaries is the old nemesis of the GFC: LIBOR.

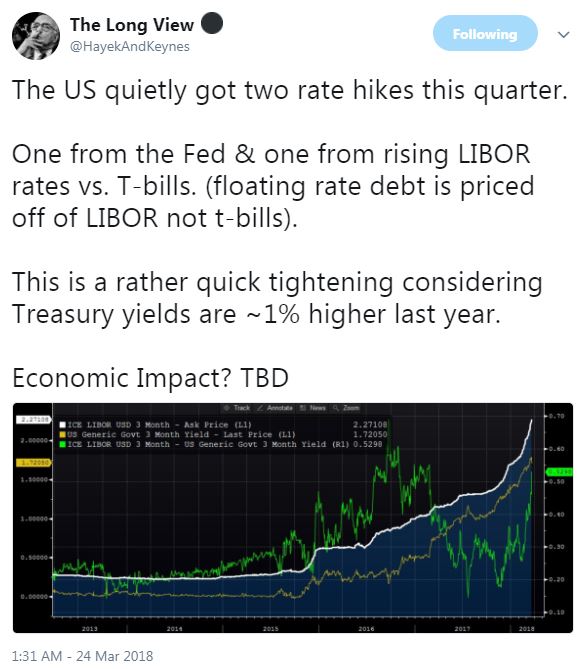

The London Interbank Offered Rate (which was literally known as ‘the fix’) has been quietly creeping up for a little while and not enough people are talking about it.

So last week’s Fed raise of 25 bps has actually had the effect of a double bump which (if it was a headline) would be front row centre to blame for market jitters.

Can’t put it any better than this tweet from terrifically insightful (and a little anonymous) @HayekAndKeynes AKA “The Long View”.

I can take a stab at the economic impact…

LIBOR is a funny thing and is destined to be replaced following the LIBOR rate-rigging scandal that has caused so much heartache. The reason it’s important is exactly as outlined above: most of the things that have a floating rate are linked to LIBOR. Mortgage debts, student debts, 90% of daily swaps, anything of relevance. So when this goes up, it has a real impact.

Now on to something I put in my last note about debt, what companies will do with their tax windfall to pay down debt and actual companies on actual exchanges that can be sold off in a heartbeat when investors are done with them? Here’s a portion:

—

“That’s an interesting swing. More companies will put the tax savings into capex but the dollar figure will actually be higher for dividends & buybacks.

OK, that’s interesting but here’s the really good bit. Only six per cent of companies are using this tax break to pay down debt.

Six. Per. Cent”

—

That was a few weeks ago. Now we’re starting to see funds get critical of companies that aren’t handling their debt.

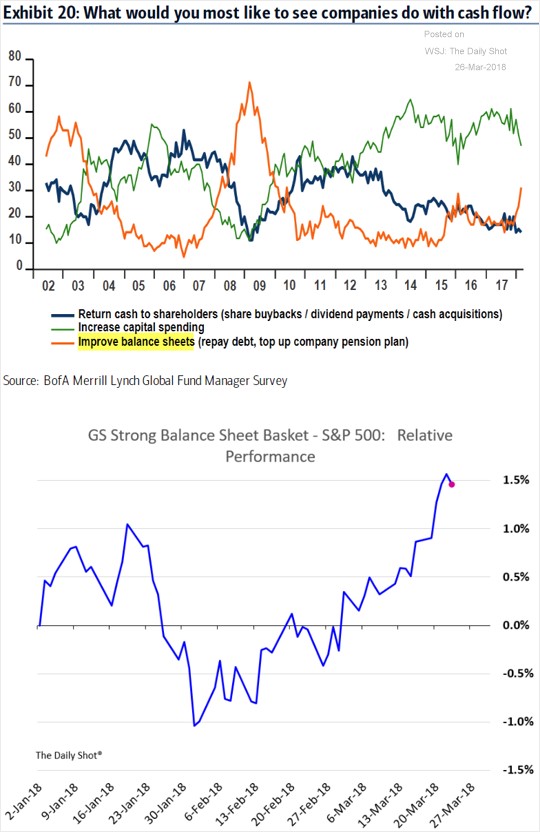

Below top chart: what fund managers would most like to see companies do with their cash flow? The orange line tells the tale.

Below bottom chart is the relative performance of “Goldman Sachs Strong Balance Sheet Basket” vs the S&P 500. You can see that companies with stronger balance sheets have been getting rewarded. Fund managers are asking the right question & companies not answering correctly are getting punished.

Courtesy WSJ’s The Daily Shot, BOFA ML.

I see no real reason why this won’t continue. Debt is a real thing and a basis point here, a basis point there and eventually you start to see some real impact to company bottom lines. Invest accordingly.

As mentioned, all of this should have been taking up the front and back pages of any and every financial journal on the planet. Were it not for this guy…

HEY KID YOU WANNA BE MY ECONOMIC ADVISOR!!??

So the headlines have been filled with Trade War discussion and I’m not sure how long it will take investors to catch on to the theme of the way Trump negotiates:

Step 1- THIS IS THE WORST POSSIBLE THING THAT CAN HAPPEN FOR ALL INVOLVED EXCEPT FOR ME.

Step 2- Your move

Step 3- Result on that deal or something completely unrelated

I’m not advocating him or this method of diplomacy, I’m just wondering how long it happens before people stop jumping out of their tree every time he does the unthinkable.

However I’m obliged to comment so here’s some points:

1. Does China or US benefit more from a Trade War? Irrelevant. To use an old quote “there are no winners in war”. The real loser is global GDP growth. Anything tied to global growth (so…everything) will be detrimented

2. USD? Lower on a Trade War. This impacts the US economy & the USD is still a little expensive.

3. Rates? In a real bind. A trade war puts the Fed’s plans on hold and changes the inflation story. Prices go up but growth slows. That’s not ideal, especially if rates do keep creeping up. The front of the yield curve moves up towards being flat, banks get crushed.

4. Hiding places? In a market correction the theme continues that there’s not that many places to hide. We’re still in a global rising rate environment and the USD might not be supported. Europe is still not favoured, more so in a trade war which impacts them too.

Best we can do is rest safe in the knowledge this all blows over soon.

Then…you know…the debt thing claims its spot on the front page.

Then it’s on…

All the best,

James Whelan & the VFS Global Macro Fund

Level 30 Australia Square, 264 George Street, Sydney NSW 2000

t +1300 220 360 | m +61 407 958 036 | www.vfsgroup.com.au/gmf

Disclaimer:

This Communication has been prepared by Vertical Capital Markets Pty Ltd (ABN 11 147 186 114 AFS Licence No. 418418) trading as VFS Group (VFS Group).

This Communication is for general information purposes only. It does not take into account your investment objectives, financial situation or particular needs. Before making an investment decision on the basis of the information contained in this report, you should consider whether the information is appropriate in light of your particular investment objectives, financial situation or particular needs. You may wish to consult an appropriately qualified professional to advise you. Derivatives can be highly leveraged, carry a high level of risk and are not suitable for all investors. Investors should only invest in such products if they have experience in derivatives and understand the associated risks.

VFS Group and/or entities and persons connected with it may have an interest in the securities the subject of the recommendations set out in this report. In addition, VFS Group and/or its agents will receive brokerage on any transaction involving the relevant securities or derivatives.

If you receive this Communication in error, please immediately delete it and all copies of it from your system, destroy any hard copies of it and notify the sender. If you are not the intended recipient, you must not disclose the information contained in this Communication in any way.