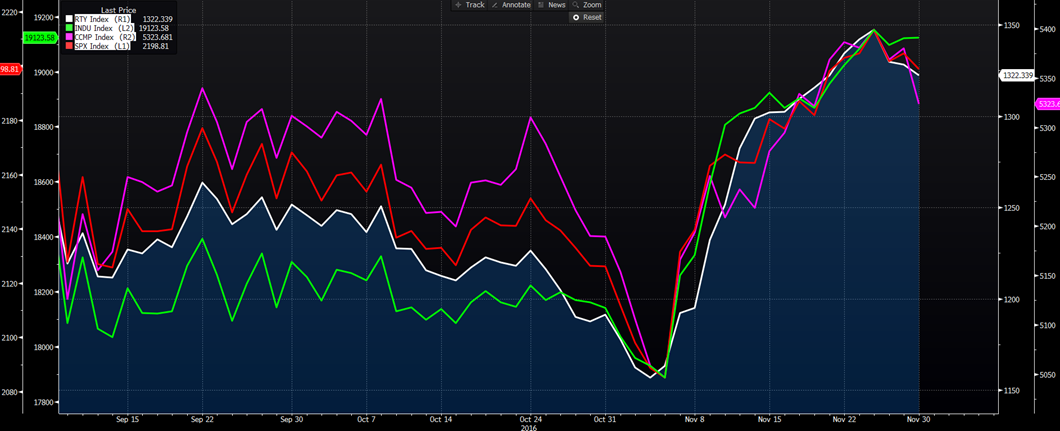

It would be remiss of us not to start this month’s Review with what was far and away the biggest event of the year, that being the election of Donald J. Trump. Four weeks ago he was given no chance of winning the Presidency with some market commentators predicting disaster to markets in the rare likelihood of his election. Today he is the President-elect with a wide range of business friendly policies ready to roll out when possible. The market reacted negatively upon seeing the first signs of Trump’s miraculous win.

Fortunately for us the lessons of Brexit were still fresh in our minds and we took the victory as another chance to be long the US market. This call was validated with all four of the major US indices reaching new highs. The small-cap Russell 2000 rose over 11% for the month, its best monthly return since October 2011.

Source: Bloomberg

Speaking objectively, we see the election of Trump as extraordinarily stimulatory to the US. In the space of three weeks, inflation has moved from being a distant hope to taking front and centre of US economic discussions. The chance of a raise in rates in the US in early December is now at 100% with raised expectations of more raising in 2017.

Put simply, November’s moves can be summarised in this way:

* Higher inflation

* Higher anticipated Fed rates

* Stronger USD

* Gold sold heavily

* Bonds sold heavily

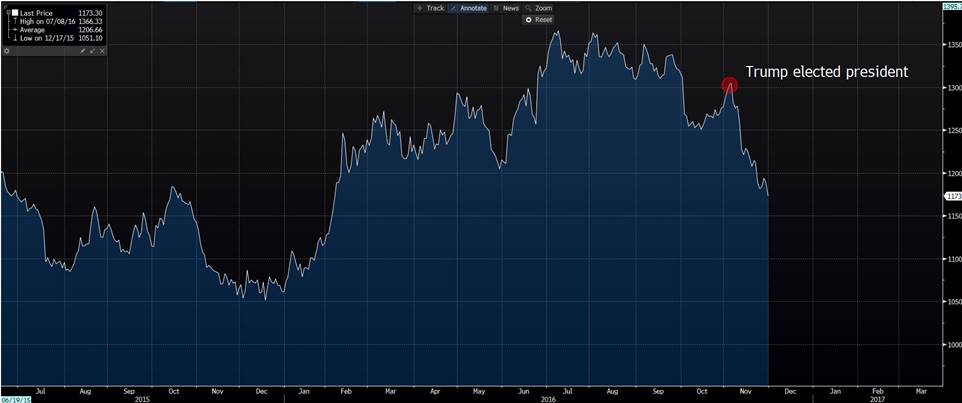

The increased anticipation of higher rates has caused a substantial rush for the exits of global bond funds and further unwinding of the ‘bond proxy’ trade. It has also caused a significant decline in the gold price. Gold, traditionally the low-inflation buy trade, has continued to fall through support levels. November saw gold in USD decline below $1200 and as much as we don’t trust big, round numbers, we still have to respect the market’s psychological barriers.

Source: Bloomberg

Speaking of psychological barriers, oil continues to trade in the range between the low $40’s and the low $50’s with the market knowing any rise in the oil price being the trigger for US shale producers to produce profitably. The month came to an end with OPEC and Russia finally reaching an agreement on production cuts. This cut is the first OPEC/Russia production cut agreement since 2001 and the market has reacted positively, with WTI rallying over 10% following the announcement.

Growth Portfolio

During the month we were relatively quiet on the growth portfolio. We have continued to hold our positions on ALQ and TPM.

Both of these positions have been volatile. In particular ALQ which saw a 15% range after it reported its figures for the quarter. In focus was its decision to close down its oil and gas operations and the market was mixed with this decision but eventually investors were comfortable with its guidance and improved forecasts of key sectors.

TPM was a speculative buy that has struggled to break out of its downward trend. Within the sector Vocus Communications once again reported poorly which has naturally weighed down TPM.

The addition of Bellamys – BAL was initially looking like a smart decision as we were seeing a solid 5% gain on the investment but this was dramatically erased as it reported poor earnings outlook and underwhelming sales figures from China’s singles day. The stock will be exited in the short term. The irony of our best trade being A2M and now our worst trade being BAL is not lost on us.

Fortunately we manage position sizes as our first level of risk management, so we expect the net effect of this position to be roughly less than 2% loss to the value of the portfolio.

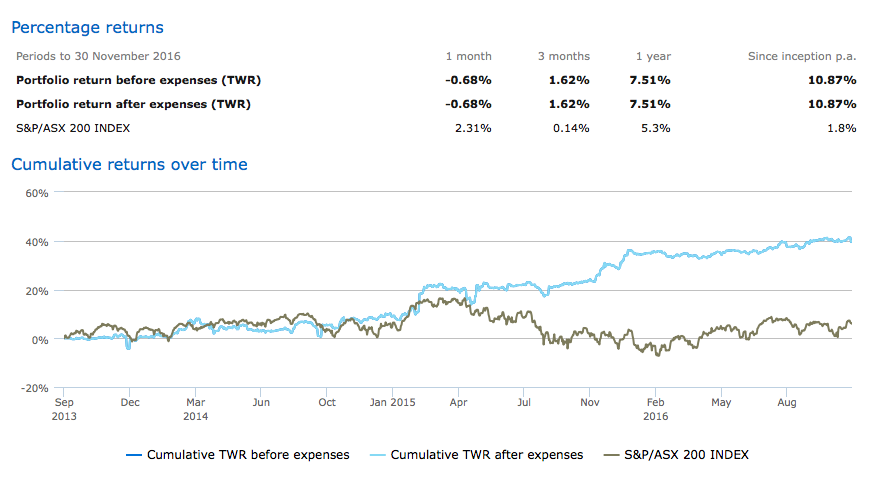

We continue to outperform the broader index by 9.07% p.a and 33.86% since inception.

Income Protected Portfolio

The month of November provided limited opportunities to add positions into our income protected portfolio, but we did however book in a very solid result on an existing position on Bank of Queensland.

We purchased the stock back in July at a price of $10.57, purchased $10.00 put options and sold an $11.26 European style call options all for November.

The $10.00 put level is our worst case scenario sale price. It is the level at which we will always have the right to sell our shares. As long as the position is open and we still own the put option, this right remains with us, in this case, until the end of November.

We elected to sell the European style calls as they can only be exercised on expiry day and as the stock was going ex-div before the November expiration date, this ensured clients were guaranteed to pick up the dividend and the franking credits.

At the time of purchasing the stock the grossed up dividend yield of BOQ was in excess of 9% which is very attractive and although the stock hasn’t performed well during the course of the year, we felt a short term rally was imminent and we were correct.

BOQ was liquidated at maximum profit with a net return of 6.5% over a 4 month period.

Annualised this is a fantastic return and all while having the downside fully protected for the life of the investment.

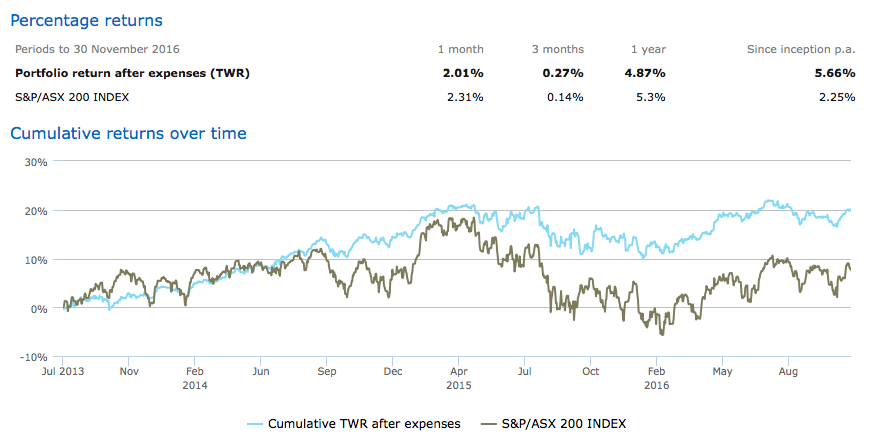

Our Income Protected Portfolio continues to outperform the market and produce consistent returns.

Options Portfolio

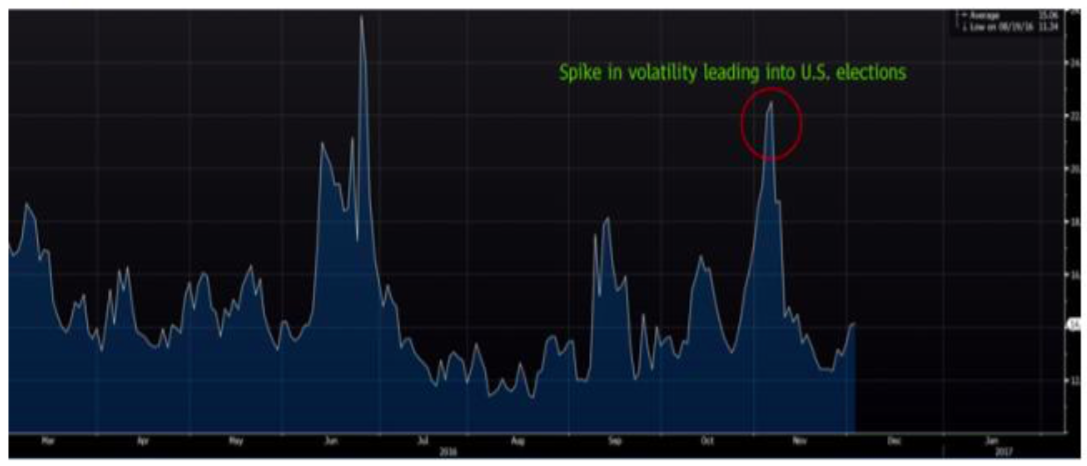

As can be expected in periods of uncertainty, we saw volatility spike and investors rushing to protect their portfolios.

Source: Bloomberg

From a trading point of view, it is this type of movement that provides us with opportunities to make short term trades with high payoffs. During the month we had some exceptional trades.

A few standout positions we managed involved selling put spreads to fund a bought call. This type of strategy is bullish but the downside is limited. We traded Santos with this strategy and managed to turn our initial investment of 13c into 46c in just over a week.

For NAB we received a credit to open the position and also to close the position. The reason this occurred was because our call appreciated quicker than the value of the sold put spread. For Telstra we achieved a similar result in just over a week – turning 5c into 20c.

Throughout this period we have had sold puts below this index and as the market has moved higher these have decreased in value, These are currently sitting over 700 points away and expire in March.

Our attempt to short RIO was the only losing trade on derivatives during the month.

On a separate note the ASX has now released weekly options over the index and selected stocks.

Disclaimer:

This Communication has been prepared by Vertical Capital Markets Pty Ltd (ABN 11 147 186 114 AFS Licence No. 418418) trading as VFS Group (VFS Group).

This Communication is for general information purposes only. It does not take into account your investment objectives, financial situation or particular needs. Before making an investment decision on the basis of the information contained in this report, you should consider whether the information is appropriate in light of your particular investment objectives, financial situation or particular needs. You may wish to consult an appropriately qualified professional to advise you. Derivatives can be highly leveraged, carry a high level of risk and are not suitable for all investors. Investors should only invest in such products if they have experience in derivatives and understand the associated risks.

VFS Group and/or entities and persons connected with it may have an interest in the securities the subject of the recommendations set out in this report. In addition, VFS Group and/or its agents will receive brokerage on any transaction involving the relevant securities or derivatives.

If you receive this Communication in error, please immediately delete it and all copies of it from your system, destroy any hard copies of it and notify the sender. If you are not the intended recipient, you must not disclose the information contained in this Communication in any way.